Why Are Card Machine Fees So High? What UK Businesses Are Actually Being Charged in 2026

If you have ever looked at your monthly statement and wondered where all the money went, you are not alone. Card machine fees are one of the most misunderstood costs in small business, and the way most providers present their pricing makes it very difficult to know whether you are paying a fair rate or being quietly overcharged.

This guide breaks down exactly how card processing fees work in the UK, what the major providers are currently charging, and what a reasonable rate actually looks like for a small or medium-sized business.

How card processing fees work: the basics

Every time a customer pays by card, a small percentage of the transaction value is taken as a fee before the money reaches your account. This is what is commonly called the card processing fee or merchant service charge.

That fee is not a single charge. It is made up of several components that get bundled together:

Interchange fee: This is the portion paid to the customer's card issuing bank. It varies depending on whether the card is debit or credit, consumer or corporate, and which scheme it belongs to (Visa or Mastercard).

Scheme fee: A small fee charged by Visa or Mastercard for use of their network.

Acquirer margin: The cut your payment provider takes on top of the above. This is where the biggest variation between providers sits.

Most providers bundle all three into a single percentage rate and present it as one simple number. That simplicity is convenient, but it also makes it very hard to see how much of that rate is genuinely covering costs and how much is pure margin.

What are typical card machine fees for UK businesses?

Rates vary significantly depending on the type of provider you are with, your monthly card turnover, and the mix of debit versus credit card transactions your customers use.

As a general benchmark for UK businesses in 2026:

Debit card transactions: reasonable rates sit between 0.35% and 0.7%

Consumer credit card transactions: reasonable rates sit between 0.65% and 1.0%

Corporate or commercial credit cards: typically higher, often 1.5% to 2.5%

If you are currently paying a flat rate above 1.75% on all transactions regardless of card type, there is a very good chance you are overpaying, particularly on debit cards which make up the majority of UK consumer payments.

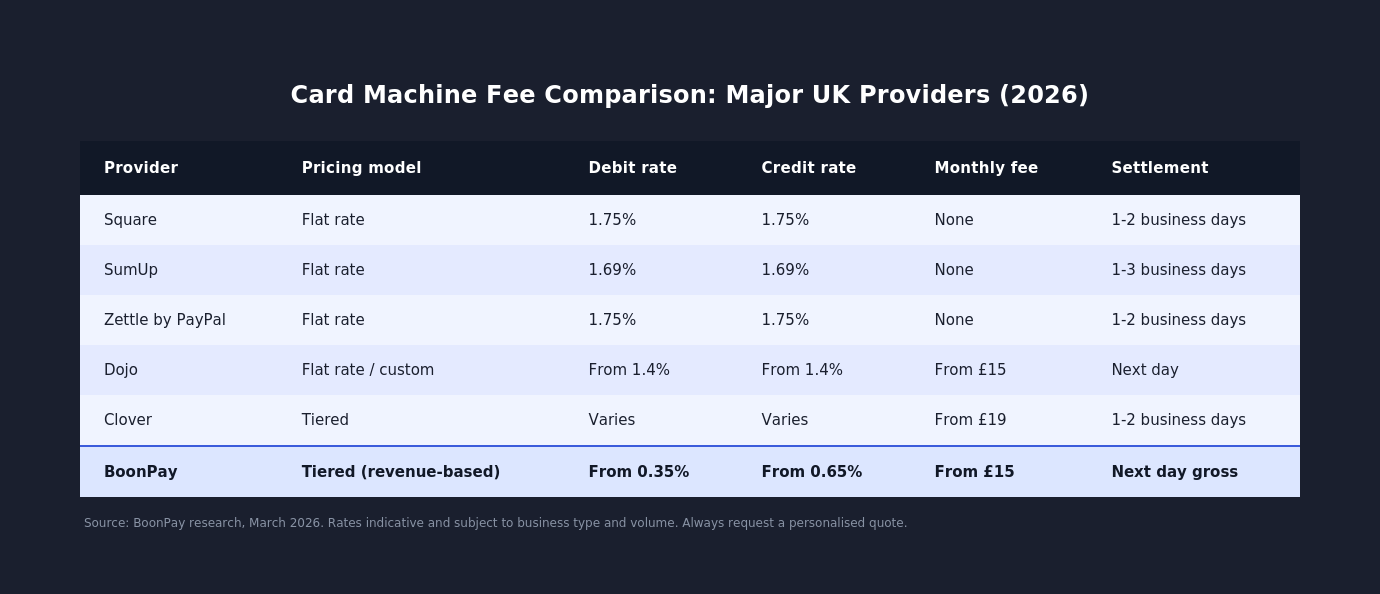

What the main providers charge: a straight comparison

Here is how the most commonly used card machine providers in the UK currently structure their fees. Bear in mind that rates can vary based on your business type and volume, so always get a personalised quote before switching.

The flat-rate providers like Square, SumUp, and Zettle are popular with new businesses and sole traders because there is no monthly fee and setup is straightforward. But the trade-off is that you pay the same percentage whether a customer taps a debit card or hands over a corporate Amex. As your monthly volume grows, that simplicity becomes expensive.

The hidden charges most businesses miss

The headline transaction rate is only part of the picture. There are several other charges that regularly catch businesses out.

PCI compliance fees: PCI DSS compliance is a requirement for any business that takes card payments, and most providers include an administration fee to cover this. It typically ranges from a few pounds to over £10 per month depending on your provider and package. It is a standard cost, but worth knowing about so it does not come as a surprise on your first statement.

Terminal rental: Many businesses rent their card machine rather than purchasing it outright, which spreads the cost and means the provider handles any hardware replacements. Terminal rental is a standard part of most packages and is worth factoring into your total monthly cost when comparing providers.

Minimum monthly service charges: Some providers charge a minimum monthly fee if your transaction volume does not reach a certain threshold. If you have a quiet month, you pay a top-up fee regardless.

Chargeback fees: If a customer disputes a transaction, you may be charged an administration fee even if the chargeback is resolved in your favour.

Early termination fees: Leaving a contract before it expires can trigger exit fees based on the remaining months of your term. Always check this before you sign.

Added together, these charges can easily add another £20 to £50 per month that never appears on your headline rate.

Why debit card rates matter more than you think

Most UK businesses assume that because debit cards are cheaper to process than credit cards, the difference is marginal. In practice, it is one of the most significant factors in your overall processing costs.

The vast majority of UK consumer card payments are made on debit cards. According to UK Finance data, debit cards account for around 80% of card transactions in the UK. If your provider is charging you the same flat rate on debit and credit, you are subsidising credit card users with every single debit payment you take.

A business processing £15,000 per month at 1.75% flat pays £262.50 in transaction fees. If 80% of those transactions are debit, a tiered pricing structure could reduce the debit portion significantly. At a blended rate closer to 0.6%, that same volume costs around £90 per month. The annual difference is over £2,000.

When does it make sense to switch pricing models?

Flat-rate pricing makes sense when you are just starting out, processing low volumes, or want the simplicity of a single number. The moment it stops making sense is usually around £5,000 to £8,000 per month in card turnover.

Above that level, tiered or revenue-based pricing almost always works out cheaper. The maths shifts in your favour because you start separating the much cheaper debit card rate from the more expensive credit card rate, rather than blending everything at a high flat percentage.

The businesses that benefit most from switching are typically hospitality and retail businesses with high debit card volumes, growing sole traders who started on a pay-as-you-go provider, and any business that has been with the same provider for more than two years without reviewing their rates.

What should you actually be paying?

A reasonable benchmark for a UK small business processing between £5,000 and £50,000 per month in card payments:

Debit card rate: 0.35% to 0.6%

Consumer credit card rate: 0.65% to 1.0%

PCI compliance and terminal rental included or clearly itemised in your monthly package

Next-day settlement as standard, not an add-on

No auto-renewing contract you did not agree to

If your current setup does not match those benchmarks, it is worth getting a comparison. The gap between what businesses pay and what they should pay is often the single largest avoidable cost in their monthly outgoings.

Find out what BoonPay would charge your business

At BoonPay, we offer tiered pricing based on your revenue, next-day gross settlement as standard, and transparent pricing with no surprises. We work with businesses across hospitality, retail, and services throughout the UK.

If you want a straight comparison against what you are currently paying, get in touch. We will look at your current statement, run the numbers, and tell you honestly what the difference would be.

Call us: 0161 394 1393 | Email: ethan@boonpay.uk | www.boonpay.uk